Last updated on July 8th, 2021 at 12:49 pm

The MICs and MPrin of a particular class of technical debt can change when we retire other seemingly unrelated classes of technical debt. In most cases, we need engineering expertise to determine technical debt retirement strategies that can exploit this property.

Financial debts usually have associated interest rates that are used to compute the periodic interest charges. Typically, the interest charge on a financial debt for a given period is the periodic interest rate multiplied by the principal, and then scaled for the length of the time period. But there are no “rates” for technical debt. Their existence would imply that MICs were proportional to the analog of “principal,” which, in the case of technical debt, is the cost of retiring the debt—the MPrin. MICs depend only weakly on the cost of retiring the debt. Instead, they depend more strongly on the impact of the debt on ongoing operations.

How financial sophistication can be a handicap

Decision makers who understand the world of financial instruments at a very sophisticated level might tend to make an understandable error. They might overvalue arguments favoring technical debt management in ways analogous to how we manage financial debts. Financial sophisticates might find appealing any argument for technical debt management that parallels financial approaches. Such programs are unlikely to work, for two reasons. First, the uncertainties associated with estimating MPrin and MICs are significant. They make technical debt management decisions more dependent on engineering and project management judgment than they are on the results of calculations and projections (see MPrin uncertainties and MICs uncertainties).

Second, the familiar concept of interest rate doesn’t apply to technical debt. For technical debt, the interest charges depend on the interaction between ongoing activities and the debt, rather than the cost of retiring the debt. And that means that MICs (and MPrin) of one class of debt can change when another class is retired.

Implications of this effect

The possibility that retiring one class of technical debt can alter the financial burdens presented by another has both favorable and unfavorable implications.

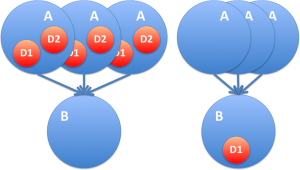

To retire D2, engineers modified B by assigning it responsibility for the tasks that formerly bore debt D2. After this change, B bears debt of type D1. Next, they retired debt D2. The right half of the figure shows the result. The system still bears debt D1. But now it’s inside B instead of A. Those modifications relieve all instances of A of both types of debt. The result is that D2 vanishes, and only a single instance of D1 remains. In this way, retiring debt D2 has reduced the MICs and MPrin for D1.

Policymakers can help

Exploiting the salutary opportunities of this property of technical debt provides an example of the risks of adhering too closely to the financial model of debt.

Many different scenarios have the property that retiring one kind of technical debt can reduce the MICs associated with other kinds. Technologists understandably tend to be more concerned with technical debt retirement strategies that emphasize short-term improvement of their own productivity. That’s why it’s so important for policymakers to provide guidance that steers the organization in the direction of enterprise benefits.